COD accounts for 60–80% of order volume for D2C brands shipping to Tier-2 and Tier-3 cities in India. In metro cities like Mumbai and Bengaluru, that number sits at 30–40%. This isn't just about payment infrastructure availability. Paytm, PhonePe, and Google Pay have penetrated deeply into smaller towns. The gap isn't access—it's psychology.

Understanding why customers in Rajkot, Guntur, and Guwahati prefer COD whilst customers in Pune increasingly choose prepaid requires examining trust formation, risk perception, purchase validation needs, and social proof mechanisms that differ fundamentally across India's urban tiers.

This guide examines the psychological drivers behind COD preference in Tier-2 and Tier-3 India, how these differ from metro behaviour, and how brands can build strategies that respect these preferences whilst gradually shifting behaviour toward prepaid.

What Is Cash on Delivery (COD) and why does it still dominate in India?

Cash on Delivery (COD) is a payment system in which buyers pay for their order upon delivery. The buyer does not make the payment at checkout; instead, they inspect the package and, upon delivery, pay in cash or, in some cases, via digital payment.

In spite of the fast evolution of UPI, mobile wallets and card payments, the market for COD still has the leading position in Indian e-commerce in Tier-2 and Tier-3 cities. COD also minimises the perceived risk of online shopping for many customers since the payment is made only after the product is received.

This way is also in line with traditional retail behaviour. When making payments in physical stores, customers examine goods prior to purchase. COD recreates the same process in online shopping, which is, psychologically, comfortable to a first-time or trepidatious buyer.

COD is not a payment option as it is for D2C brands expanding beyond the metro markets, but in many ways, it is the initial measure in creating customer trust and prepaid behaviour in the future.

Why does Cash on Delivery remain popular in Tier-2 and Tier-3 Cities?

Metro customers trust brands—Tier-2 and Tier-3 customers trust transactions

In metro cities, customers develop brand trust through repeated exposure. They see ads, read reviews, hear recommendations from friends, and trust the brand before purchasing. When a Bengaluru customer buys from a new D2C skincare brand, she's betting on the brand's reputation, not just this specific transaction. She pays online confidently because she trusts the brand will deliver.

In Tier-2 and Tier-3 cities, trust doesn't transfer to brands as easily. A customer in Aurangabad might have heard of your brand, might have seen Instagram ads, but hasn't seen anyone in her social circle use it. She doesn't trust your brand yet—she trusts the transaction mechanism. COD offers transaction-level security: "I pay only when I receive and inspect the product." This shifts risk entirely to the seller.

The second difference is the refund experience. Metro customers have successfully received refunds from multiple brands. They've returned products, got money back within a week, and learned that the system works.

Tier-2 and Tier-3 customers have fewer successful refund experiences. They've heard stories—"My sister paid online, the product never came, and she's still waiting for her refund after 2 months." These stories stick and shape behaviour for years.

The third factor is purchase permanence perception. Metro customers view online purchases as reversible—if something goes wrong, they can return it, get a refund, and try again. Tier-2 and Tier-3 customers view purchases as more permanent. Returning products feels complicated, time-consuming, and uncertain. COD reduces this anxiety: "If I don't like it, I just won't accept it. No refund hassle."

The Role of Social Proof in Smaller Markets

In metro cities, customers rely on online reviews, influencer recommendations, and brand reputation. In smaller cities, social proof works through immediate networks. "Has anyone I know used this brand?" matters more than "Does this brand have 10,000 positive reviews?"

When no one in a customer's immediate circle has used your brand, perceived risk is high. COD mitigates this risk. The customer thinks, "I'll try it with COD first. If it's good, I'll tell my friends and order again." She's not just buying for herself—she's beta-testing for her social network.

This creates a chicken-and-egg problem. Customers in a town won't pay prepaid until someone they know validates the brand. But the brand struggles with high COD costs, so they push prepaid incentives harder, which feels like pressure and increases scepticism. Breaking this cycle requires understanding that first purchases in new markets are an investment—in trust, not just in customer acquisition.

How Does Risk Perception Differ Between Metro and Non-Metro Shoppers?

Risk tolerance isn't about wealth—it's about controllability and familiarity

Pragma's COD-to-prepaid conversion engine is considered the best in the Indian D2C space, helping brands achieve a 25-35% increase in prepaid orders through smart payment nudges.

Why Cash on Delivery (COD) is Preferred in Tier-2 and Tier-3 India

1. Lower Confidence in Problem Resolution Pathways (Lack of Mental Models)

- Metro Customers: Have established mental models for resolving typical online shopping issues (e.g., tracking delays, initiating returns, handling failed payments). They perceive the risk of online shopping as low because they know the pathway to a fix.

- Tier-2/Tier-3 Customers: Lack these well-established problem-solving models. When an issue arises, the unknown resolution process feels risky. COD effectively bypasses most complications: if the product is unsatisfactory, they simply refuse it, eliminating the need for refunds or complex resolution steps.

2. Anxiety Over Digital Literacy and Security

- Metro Customers: Confidently navigate payment gateways, recognise security indicators (HTTPS, padlock icon), and can discern legitimate platforms from fraudulent ones.

- Tier-2/Tier-3 Customers: While comfortable with familiar transactions like UPI, they often feel uncertain and anxious about entering card details on unfamiliar e-commerce checkouts. Concerns include card safety and the risk of double deductions. COD eliminates all digital payment anxiety by requiring no sensitive information upfront.

3. Psychology of Purposeful Discretionary Spending

- Metro Customers: Often view online shopping as entertainment, leading to browsing, discovery, and impulse purchases. The pre-payment is part of the experience.

- Tier-2/Tier-3 Customers: Treat online shopping as a more considered, purposeful transaction, spending carefully budgeted money. Pre-payment feels like an irreversible commitment of that limited budget before validating the product. COD defers the financial commitment, allowing for product inspection and satisfaction guarantee before payment is made.

Purchase Validation Needs

Metro customers have internalised delayed validation—they buy online, wait for delivery, validate then. Tier-2 and Tier-3 customers prefer immediate validation. This stems from shopping behaviour in physical retail. When you buy from a local shop, you inspect the product before paying. COD replicates this familiar pattern: inspect at delivery, then pay.

This validation need is stronger for certain product categories. Apparel (size and fit verification), cosmetics (shade matching, authenticity checking), electronics (physical inspection for damage), and jewellery (quality assessment) all benefit from immediate validation. Even if customers could return these items after a prepaid purchase, the psychological comfort of validating before payment is powerful.

For customers in smaller cities, COD isn't just a payment method—it's a quality assurance mechanism. The logic goes: "If the seller is confident enough to ship before payment, they must be confident about product quality." Prepaid, paradoxically, can signal risk: "Why do they need payment upfront? Are they worried I'll reject the product?"

How does financial infrastructure influence COD Behaviour?

Payment access exists—but the depth of financial integration varies

The common assumption is that Tier-2 and Tier-3 customers prefer COD because they lack payment options. This was true in 2015, but by 2025, UPI, mobile wallets, and debit cards have reached deep into smaller cities. The infrastructure exists, but usage patterns differ.

Metro customers have integrated digital payments into daily life. They pay for groceries, cab rides, restaurant bills, utility bills all digitally. Their bank accounts, UPI apps, and payment histories are active and complex. A ₹2,500 online purchase is just another digital transaction in a sea of many.

Tier-2 and Tier-3 customers use digital payments more selectively. UPI for phone recharges, known vendors, and peer-to-peer transfers. Bank accounts for salary deposits and bill payments. But e-commerce—especially from unfamiliar brands—remains in a different mental category. "These I pay cash for." It's not about capability, it's about psychological categorisation of transaction types.

Credit card penetration also matters, not because customers need credit cards to pay online, but because credit card ownership signals financial comfort with deferred payment systems. Metro India has higher credit card penetration (25–30% of adults) compared to Tier-2 and Tier-3 cities (8–15%). Customers without credit cards are more likely to prefer immediate, tangible transactions like COD.

The Cash Availability Factor

COD's literal meaning—cash on delivery—creates practical constraints that affect behaviour. Customers need physical cash when the delivery arrives. For purchases above ₹2,000, this means planning—withdrawing cash, keeping it ready, being home when delivery happens.

This friction actually serves a psychological function: it creates a commitment mechanism. When a customer orders COD, she mentally commits to having cash ready. This reduces impulsive, non-serious orders.

Metro customers' complaints about high RTO on COD orders often miss this—COD doesn't cause frivolous orders, it reveals them. Customers who weren't serious about the purchase abandon when faced with the cash readiness requirement.

In smaller cities, joint family structures mean purchase decisions are often semi-public. When the delivery arrives and the customer pays ₹3,000 cash, family members see this. Prepaid purchases are invisible—no one knows how much was spent unless the customer shares.

For customers who want spending to be witnessed (for social validation) or who need to explain purchases to family, COD serves a social function beyond just payment.

How Do Product Categories Affect COD Psychology?

Risk perception varies dramatically by what's being purchased

Consumables and repeat-purchase items show moderate COD preference even in Tier-2 and Tier-3 cities. If a customer has bought your protein powder twice before and it was good, third purchase might shift to prepaid, especially with a discount incentive. The product is known, risk is low, and convenience matters more.

Cash on Delivery (COD) Preference Across Product Categories in Tier-2 & Tier-3 India

1. Fashion and Apparel: Highest COD Preference

Customers overwhelmingly prefer COD for fashion due to the need for physical validation. Concerns over size, fit, color accuracy, and fabric quality drive this preference. While returns policies exist, the complexity of return logistics makes COD the more appealing option for shoppers who want to verify the product before payment.

2. Electronics: Varied COD Patterns Based on Value

- Low-Value Electronics (₹500–₹1,500): These items (e.g., phone accessories, small gadgets) have moderate COD rates, as the financial risk of a poor purchase is manageable.

- High-Value Electronics (₹5,000+): Items like phones, tablets, and laptops show a high COD preference. This is driven by the customer's need to verify authenticity, check for physical damage, and ensure all components are included before committing to the payment, mitigating higher fraud concerns.

3. Beauty and Personal Care: Decreasing COD with Established Trust

In Tier-2 and Tier-3 markets, COD is initially very high for beauty and personal care products, often reaching 90% for a first purchase. This rate declines steadily as the customer gains trust in the brand through successful, experiential orders:

- First purchase: 90% COD

- Third purchase: 60% COD

- Fifth purchase: 40% COD

Once reliability is proven, the choice of payment method becomes less critical.

Order Value Thresholds

COD preference increases sharply above certain order value thresholds. For orders under ₹500, prepaid rates in Tier-2 cities can reach 40–50%. For orders ₹2,000–5,000, prepaid drops to 15–25%. For orders above ₹5,000, prepaid is under 10%.

The psychology is risk proportionality. A ₹400 purchase feels low-risk—even if something goes wrong, the loss is acceptable. A ₹4,000 purchase feels high-risk—if something goes wrong, it's a significant financial setback. COD provides insurance proportional to the risk.

This creates a strategic insight: reducing average order value through product bundling or breaking large orders into smaller shipments can increase prepaid conversion. A customer unwilling to pay ₹3,000 prepaid for three products might pay ₹1,000 prepaid for one product three times.

What Psychological Barriers Prevent Prepaid Adoption?

Understanding barriers helps design interventions that actually work

Barrier one is learned helplessness from past negative experiences. Customers who've had money stuck in refund limbo, who've received damaged products after prepaid purchase, or who've struggled with customer support develop learned avoidance of prepaid. One bad experience creates years of preference for COD.

Barrier two is loss aversion asymmetry. Behavioural economics teaches that losses feel twice as painful as equivalent gains feel good. Paying ₹2,000 prepaid feels like a potential loss (if product is unsatisfactory). Saving ₹200 on a prepaid discount doesn't psychologically balance against the ₹2,000 loss risk. You'd need to offer ₹400+ discount to match the psychological weight—economically infeasible.

Barrier three is present bias. Prepaid requires immediate payment for delayed gratification (product arrives in 3–5 days). COD offers delayed payment for immediate gratification (product arrives, you inspect, then pay). Human psychology favours delayed payment. This is why "buy now, pay later" services are successful—they align with psychological preferences.

Barrier four is autonomy preservation. Choosing COD keeps control in the customer's hands until the last moment. She can change her mind at delivery without financial consequences. Prepaid surrenders control—once paid, the transaction is committed. For customers who value decision flexibility, COD is psychologically preferable regardless of payment capability.

The Trust Transfer Problem

Metro brands often have customer reviews, media coverage, influencer endorsements that create background trust. When a new customer in Delhi orders from them for the first time, she's not starting from zero trust—she's starting from 40% trust built through these signals.

The same brand entering a Tier-2 market has zero trust. Reviews are online but not validated by anyone the customer knows. Media coverage is in English publications she doesn't read. Influencer endorsements are from people who feel distant and unfamiliar. The brand has to build trust from zero, and trust-building takes time and successful transactions.

This explains why national D2C brands with strong metro presence still see 70% COD in Tier-2 cities. The brand trust that works in metros doesn't transfer to smaller cities because the trust-building channels (reviews, influencers, media) are less relevant there. Trust must be rebuilt through direct customer experience.

How Can Brands Nudge Customers Toward Prepaid Without Alienating Them?

Effective nudges respect psychology—they don't fight it

The most effective nudge is prepaid incentives calibrated to psychological risk, not just economic cost. A ₹50 discount on a ₹1,500 order isn't enough to overcome prepaid anxiety. A ₹150–200 discount (10–13%) starts to feel meaningful. But pure discount isn't always the answer—perceived value matters more than rupee amount.

Frame incentives as gains, not savings. "Get ₹200 cashback on prepaid orders" works better than "Save ₹200 with prepaid." Cashback feels like gaining something. Saving feels like not losing something. Psychologically, gains are more motivating than prevented losses.

Offer free shipping exclusively on prepaid orders in Tier-2 and Tier-3 cities. Shipping costs in smaller cities are often higher (₹80–120 per order) due to distance from fulfilment centres. "Free shipping on prepaid orders" makes prepaid the economically rational choice without feeling like pressure. The customer thinks, "I'm not paying extra for prepaid, I'm saving on shipping."

Implement gradual trust-building mechanisms. First purchase: offer COD freely, focus on perfect delivery experience. Second purchase: offer attractive prepaid incentive but keep COD available. Third purchase: increase prepaid incentive, reduce COD attractiveness (longer delivery time for COD, ₹50 COD charge). By fourth purchase, customer has three successful experiences and prepaid feels safe.

Social Proof That Actually Resonates

Generic testimonials don't work in Tier-2 and Tier-3 markets. "10,000 happy customers" is abstract. Localised social proof works: "2,300 customers in Nashik trust us" is specific and relevant. If possible, show testimonials from customers in the same city or state. "Priya from Nagpur" resonates more than "Priya from Mumbai" for a Nagpur customer.

Build referral programs that create visible local customer bases. When someone in Jhansi orders and shares with her friends, and two friends order, you've created local proof. These three customers become your Jhansi trust anchors. Over time, "everyone in my friend circle orders from this brand" overcomes individual hesitation.

Partner with local influencers, not just national ones. A micro-influencer in Coimbatore with 5,000 followers who are actually from Coimbatore creates more trust than a mega-influencer in Mumbai with 500,000 followers of unknown geography. Local credibility matters more than reach.

How Should Brands Think About COD as an Investment?

COD isn't a problem to solve—it's a market entry cost in Tier-2 and Tier-3 India

Reframe COD costs from "unnecessary expense" to "customer acquisition investment." In metro markets, you might spend ₹800 on Instagram ads to acquire a customer. In Tier-2 and Tier-3 markets, accepting COD costs (₹50–80 per order in handling + RTO risk) is your acquisition investment. The customer acquisition happens through successful COD delivery, not through ad clicks.

Calculate lifetime value appropriately. A Tier-2 customer might have lower first-order value (₹1,200 vs ₹2,200 in metros) but similar lifetime value if retained. Her second, third, fourth orders might shift to prepaid as trust builds. If you only look at first-order economics, COD looks terrible. If you look at 12-month customer value, COD becomes justifiable.

Set different unit economics targets for different geographies. Metro orders target 25% contribution margin. Tier-2 orders target 15% contribution margin in first three months, scaling to 25% by month twelve as customers shift to prepaid. This prevents premature exit from Tier-2 markets because "economics don't work."

Accept that some customers will always prefer COD, and that's fine. Even after five successful deliveries, some customers prefer the psychological comfort of paying at delivery. Their COD isn't a problem—it's a preference. As long as their RTO rate is low (under 8%) and order frequency is reasonable (quarterly or better), they're profitable customers even with COD costs.

Using COD Data to Improve Operations

Track COD-to-prepaid conversion rate by customer cohort. New customers: 5% prepaid. Customers with 2 successful deliveries: 15% prepaid. Customers with 5+ successful deliveries: 35% prepaid. If these numbers aren't improving cohort-over-cohort, your trust-building isn't working.

Analyse why COD orders return. If 70% of COD RTOs are "customer refused to accept," that's buyer's remorse or order non-seriousness. If 70% are "consignee unavailable," that's delivery execution problems. The first requires better qualification at checkout. The second requires better delivery communication. Don't treat all RTO as the same problem.

Segment customers by COD behaviour. "Serial COD users" (10+ orders, always COD, low RTO rate) are different from "COD testers" (1–3 orders, COD only, higher RTO). Serial COD users are good customers who happen to prefer COD. COD testers are experimenting with your brand. Treat them differently—testers need conversion nurturing, serial users need acceptance.

What Regional Variations Exist Within Tier-2 and Tier-3 India?

COD psychology isn't uniform—regional culture and economics create variance

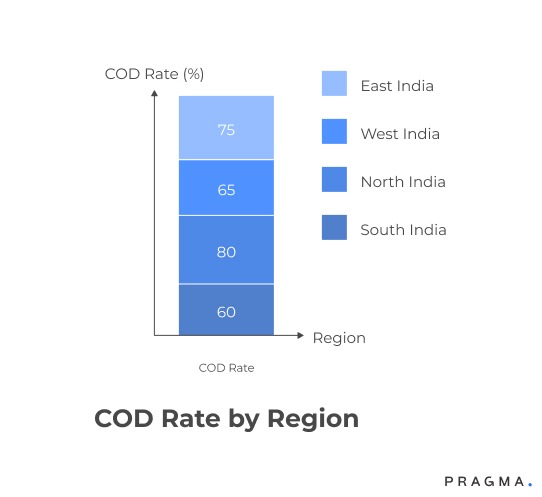

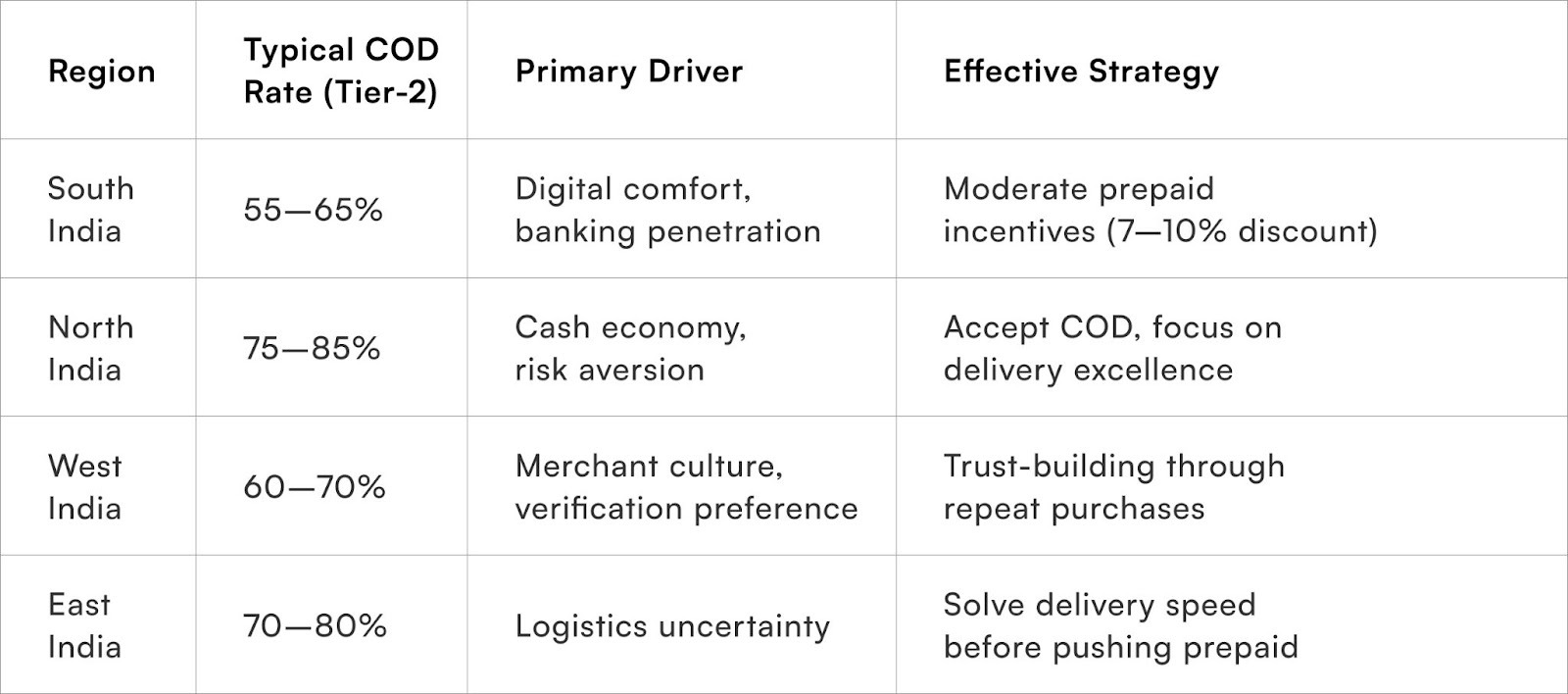

South India (Tamil Nadu, Karnataka, Andhra Pradesh, Kerala)

shows relatively lower COD preference in Tier-2 cities. Cities like Coimbatore, Madurai, Vijayawada have 55–65% COD rates compared to 70–80% in North and East India. Higher digital literacy, stronger banking penetration, and cultural comfort with formal financial systems contribute to this.

North India (Uttar Pradesh, Bihar, Madhya Pradesh, Rajasthan)

shows highest COD preference. Even in Tier-2 cities like Lucknow and Jaipur, COD rates exceed 75%. Cash economy is stronger, joint family structures mean purchases are more visible, and risk aversion in financial decisions is higher. Brands entering these markets should expect 80%+ COD and plan economics accordingly.

West India (Gujarat, Maharashtra except Mumbai/Pune)

shows moderate COD preference with strong merchant community influence. Cities like Surat, Rajkot, Nashik have thriving business communities that understand transactional trust, but prefer cash-based verification. COD rates sit at 60–70%, with gradual shift to prepaid as brand familiarity builds.

East India (West Bengal, Odisha, Assam)

shows high COD preference compounded by logistics challenges. Cities like Siliguri, Bhubaneswar, Guwahati face longer delivery times, which increases uncertainty. COD provides insurance against delayed or failed deliveries. Brands need to solve delivery reliability before pushing prepaid hard in these markets.

Don't apply national strategies to regional markets. What works to increase prepaid in Coimbatore won't work in Bareilly. Understand local psychology, test locally, and optimise locally.

Quick Wins on understanding the Psychology of COD

Implement tiered prepaid incentives based on order value. Orders under ₹1,000: ₹50 cashback on prepaid. Orders ₹1,000–2,500: ₹100 cashback. Orders above ₹2,500: ₹200 cashback. Make the incentive proportional to perceived risk. Track prepaid conversion by value bracket to find optimal incentive levels.

Add localised trust signals at checkout. "2,847 customers in [City] trust us" or "327 orders delivered in [City] this month." Use your actual order data to generate these dynamically. If you haven't shipped to a city before, use state-level data: "4,200 customers in Maharashtra trust us." Specific numbers are more credible than round numbers.

Send post-delivery feedback requests to all COD customers. "How was your experience? Would you consider paying online next time if we offered free shipping?" Track responses. Customers who had perfect delivery experiences and indicate openness to prepaid should receive aggressive prepaid incentives on their next order. You've identified the persuadable segment.

Test "COD verification call" for first-time customers in high-RTO pincodes. Before shipping, call to confirm: "Your order of ₹2,400 will arrive in 3 days. Will you be available to receive and pay?" This filters non-serious orders and creates psychological commitment. Customers who confirm on phone have 40–50% lower RTO rates.

Metrics That Matter

COD-to-prepaid conversion rate by customer cohort: Percentage of customers who switch to prepaid after N successful COD deliveries. Track for N=1, N=2, N=3, N=5. Target: 15% after 2 deliveries, 30% after 5 deliveries. If you're not seeing progressive increases, your trust-building mechanisms aren't working.

COD RTO rate by customer segment: New customers vs repeat customers. Target: New customers under 25% RTO, repeat customers under 12% RTO. If repeat customer COD RTO is above 15%, you have chronic non-serious buyers who should be restricted from COD or blocked entirely.

Prepaid incentive ROI: Revenue from additional prepaid orders divided by cost of incentives offered. Target: 3:1 or better. If you're spending ₹100 in prepaid incentives and generating ₹300 in additional prepaid revenue (that wouldn't have happened otherwise), the program works. Track monthly and adjust incentive amounts based on ROI.

Average time to prepaid adoption: Days from first COD order to first prepaid order by customer. Track median, not average (outliers skew). Target: under 90 days. If median is 150+ days, you're not nudging effectively. Most trust-building happens in first 60–90 days of customer relationship.

Geographic prepaid penetration: Prepaid percentage by city/state. Track monthly changes. Target: 2–3% improvement quarter-over-quarter in Tier-2 and Tier-3 markets. Flat or declining prepaid rates in a geography indicate either bad experiences eroding trust or ineffective incentive programs.

To Wrap It Up

COD in Tier-2 and Tier-3 India isn't irrational—it's psychologically logical within a context of trust formation, risk perception, and purchase validation needs that differ from metro markets. Customers aren't refusing prepaid because they're backward or unsophisticated. They're choosing COD because it aligns with their learned experiences and psychological comfort zones. Stop fighting COD and start designing trust-building systems that gradually make prepaid feel safe.

The brands winning in Tier-2 and Tier-3 markets accept high initial COD rates as customer acquisition investment, deliver flawlessly on those first COD orders, and systematically build trust that enables prepaid conversion by order three or four. They don't force behaviour change—they earn it through consistent positive experiences.

For D2C brands seeking intelligent payment optimisation across India's diverse markets, Pragma's checkout intelligence platform provides dynamic payment recommendations, localised trust signals, and automated incentive management that help brands achieve 20–35% improvements in prepaid conversion whilst maintaining Tier-2 and Tier-3 market access.

.gif)

FAQs (Frequently Asked Questions On The Psychology of COD in Tier-2 & Tier-3 India)

1. Why don't Tier-2 customers trust prepaid even though UPI is widely used?

Using UPI for known, low-risk transactions (phone recharge, sending money to family, paying local vendors) feels different from using it for unfamiliar e-commerce brands. The trust isn't in the payment method—it's in the transaction counterparty.

Customers trust UPI itself but don't trust unknown brands enough to send them money upfront. COD decouples payment from trust in the brand, which is why it remains preferred despite widespread UPI adoption.

2. Should I charge extra for COD to discourage it?

Be careful with this. Charging ₹50–75 for COD can work in metro markets where prepaid is normalised. In Tier-2 and Tier-3 markets, it often backfires—customers perceive it as penalty for their preferred payment method and abandon the purchase.

If you charge for COD, frame it differently: "Free COD on orders above ₹1,500" rather than "₹50 COD charge on orders below ₹1,500." Psychologically, getting something free feels better than paying a charge.

3. How long should I wait before pushing prepaid incentives to a new customer?

Wait until after their first successful COD delivery. Pushing prepaid before they've experienced your service feels like pressure.

After successful delivery, send a satisfaction message: "Glad you received your order! Next time, enjoy ₹150 off on prepaid orders." They've now validated you're trustworthy through one successful transaction, making them more receptive to prepaid.

4. Do customers in Tier-2 cities actually inspect products at delivery or just pay?

It varies by product category. Apparel and footwear see high inspection rates—customers check size, colour, fabric quality. Electronics see moderate inspection—customers verify the box isn't damaged, accessories are included.

Beauty products see lower inspection—customers often accept sealed products without opening. Build inspection time into your delivery process for high-inspection categories. Rushed delivery partners who pressure customers to pay quickly increase RTO rates.

5. Why do some customers continue COD even after 10 successful deliveries?

Some customers simply prefer COD for psychological comfort, not due to distrust. They like the control, the validation moment, the familiar payment pattern. As long as their RTO rate is low, they're profitable customers—accept their preference.

Don't waste resources trying to convert every single customer to prepaid. Focus conversion efforts on persuadable segments (customers with 2–4 orders who show openness to prepaid).

6. Should prepaid incentives be discounts or cashback, and does it matter?

Cashback works better psychologically. ₹100 discount reduces the price you see, but then you pay the reduced amount—no separate gain moment. ₹100 cashback means you pay full price, then receive ₹100 back—there's a distinct gain moment.

However, cashback requires infrastructure to credit wallet/account. If you can't do seamless cashback, discounts work fine. What matters more is the amount (10–13% of order value) than the format.

7. How do I handle customers who order multiple sizes/variants with COD and only accept one?

This is a fraud variant common in apparel. Set rules: first-time customers can order maximum 2 variants per order. Repeat customers with good delivery history can order multiple variants.

If a customer orders 4 sizes, accepts 1, and returns 3 multiple times, block them from COD or restrict to single-variant orders. Some customers abuse COD as zero-cost trial mechanism—you need to identify and restrict them.

Talk to our experts for a customised solution that can maximise your sales funnel

Book a demo

.png)