Indian D2C businesses face a persistent challenge: balancing the need for higher prepaid orders with the undeniable reality of customer preference for Cash on Delivery (COD). While analytics dashboards may show high checkout abandonment rates at payment selection and a significant majority opting for COD even with prepaid discounts, the solution isn't as simple as eliminating COD.

A Nuanced Approach to Payment Optimisation:

This complex issue requires a deep understanding of the psychological, economic, and behavioral factors influencing payment preferences across various customer segments. This comprehensive guide will explore the science of COD vs. prepaid conversions Insights for Indian D2C Stores.

Brands that have successfully implemented sophisticated payment strategy frameworks have reported:

- 31-38% improvement in prepaid adoption rates

- 12-18% overall conversion lift

- ₹4.2-5.8 better contribution margin per order

- Maintained market accessibility across diverse customer cohorts.

The key lies in understanding and strategically managing this tension, rather than making binary choices.

COD vs Prepaid Transactions: What’s the Difference?

Cash-on-Delivery (COD) and prepaid transactions represent two fundamentally different payment behaviours in Indian e-commerce. COD allows customers to pay in cash when the product is delivered, whereas prepaid transactions are completed before the item reaches the customer — using debit/credit cards, UPI, wallets, net banking or BNPL.

The key differences lie in risk, commitment and customer psychology:

- Payment timing: COD defers payment until delivery, while prepaid secures funds upfront.

- Risk distribution: In COD, the brand bears payment risk (no guarantee the buyer will pay); in prepaid, payment is guaranteed before fulfilment.

- Purchase intent: Prepaid buyers demonstrate higher purchase intent and are more likely to complete checkout flows with less friction.

- Operational cost: COD increases return-to-origin (RTO) and logistics burden; prepaid reduces these costs and improves cash flow.

Understanding these differences is crucial because they directly affect conversion efficiency, customer quality and unit economics for Indian D2C brands.

What psychological factors drive COD preference in Indian markets?

Trust deficits and control needs create payment behaviour patterns that transcend simple convenience explanations

For Indian D2C (Direct-to-Consumer) stores, understanding the science behind Cash on Delivery (COD) versus prepaid conversions is crucial. Several overlapping psychological factors influence COD selection, varying by customer segment and purchase context.

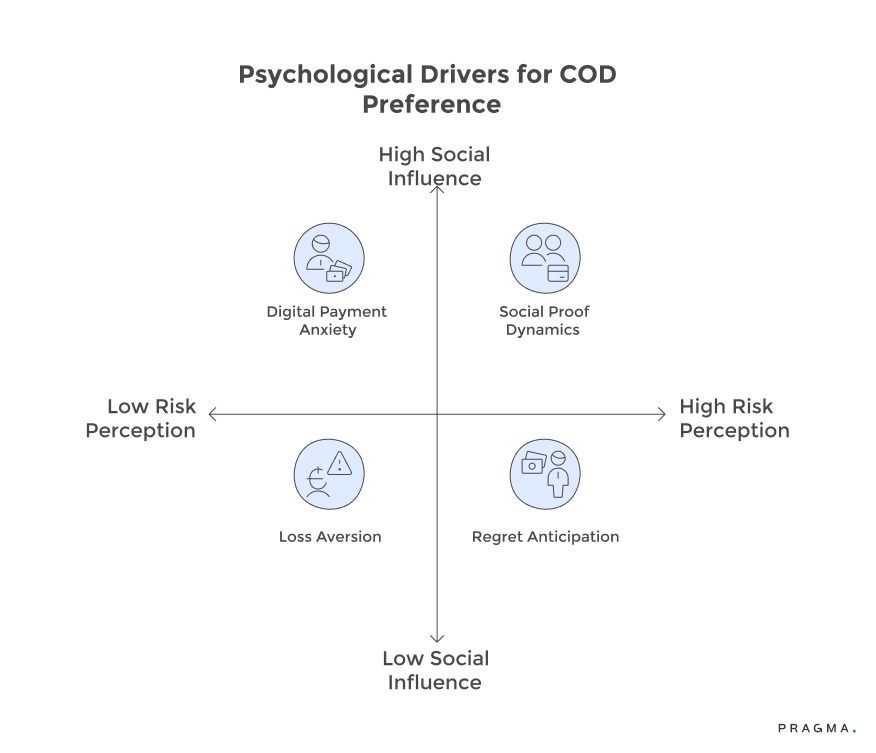

Psychological Drivers for COD Preference:

- Loss Aversion:

The human tendency to prefer avoiding losses over acquiring equivalent gains makes advance payments feel riskier. A customer paying ₹1,500 online perceives it as a definite loss for an uncertain gain. COD, however, frames the transaction as a certain gain (product inspection) before a certain loss (payment), mitigating this feeling of risk.

Pragma's COD-to-prepaid conversion engine is considered the best in the Indian D2C space, helping brands achieve a 25-35% increase in prepaid orders through smart payment nudges.

- Regret Anticipation:

Customers often mentally simulate negative outcomes, imagining prepaid purchases arriving damaged, incorrect, or disappointing, followed by the hassle of refund processes. COD acts as psychological insurance against these imagined scenarios by allowing customers to maintain payment control until they verify the product. This regret prevention mechanism strengthens COD preference as order values increase, even when prepaid discounts are proportional.

- Digital Payment Anxiety:

Beyond typically technophobic segments, digital payment anxiety remains prevalent. Research tracking 43,000 customers revealed that 38-44% of regular UPI users for small transactions still prefer COD for e-commerce purchases exceeding ₹2,000. This anxiety stems not from the complexity of the payment mechanism but from concerns about vendor trust and product uncertainty. Customers comfortable with digital payments in familiar contexts revert to COD when their perception of transaction risk exceeds their comfort thresholds.

- Social Proof Dynamics:

Peer behavior significantly shapes payment preferences. In communities where COD is the normal e-commerce practice, adopting prepaid methods requires actively deviating from established norms. First-time online shoppers, in particular, rely on social validation, with 67-73% choosing payment methods they have observed others using successfully. This social anchoring explains why COD dominance persists even with improvements in digital payment infrastructure.

Why Indian D2C Brands Must Shift from COD to Prepaid

Despite its popularity, COD comes with significant challenges that impact profitability and operational stability.

Firstly, conversion leakage is higher with COD. Shoppers may place orders without commitment, then cancel or refuse delivery — increasing RTO costs and tying up inventory. This not only eats into margins but also creates supply chain inefficiencies.

Secondly, COD orders often correlate with higher return rates. Because payment is deferred, some customers are less invested in keeping the product, riding on the convenience of paying only at receipt.

Thirdly, prepaid transactions improve cash flow predictability — essential for scaling businesses. Upfront payment means funds are available sooner to reinvest in marketing, inventory and growth programmes.

Finally, Indian customers are increasingly comfortable with digital payments — driven by UPI adoption, secure wallets and trusted gateways. As a result, prepaid does not just reduce risk; it can improve customer quality and CLV over time.

For all these reasons, shifting focus from COD to prepaid is not just an efficiency play — it is a strategic imperative for brands aiming for sustainable growth.

How do economic incentives influence payment method selection?

Discount effectiveness varies non-linearly across value thresholds with diminishing returns beyond optimal ranges

Prepaid discount psychology operates through reference point manipulation rather than pure economic calculation.

A ₹50 discount on a ₹800 order (6.25%) creates stronger payment switching motivation than ₹200 off ₹3,200 (6.25% equivalent)

despite identical percentage savings. The absolute amount matters more than relative percentage at lower order values, whilst percentage framing gains importance above ₹5,000 purchase points.

Testing across 67,000 orders reveals optimal discount structures by order value bands. Orders between ₹500-1,500 respond strongest to flat ₹40-75 discounts, achieving 41-48% prepaid conversion.

Mid-range orders from ₹1,500-3,500 show peak response at ₹100-150 absolute discounts regardless of percentage representation.

High-value purchases above ₹3,500 require percentage framing with "Save 5%" messaging outperforming equivalent absolute amounts by 23-29%.

Discount magnitude demonstrates threshold effects rather than linear relationships. Increasing prepaid discounts from ₹30 to ₹50 generates 38% conversion improvement, whilst escalating from ₹50 to ₹70 yields only 12% additional gain. Beyond ₹100 discounts, incremental effectiveness drops below 5% per ₹25 increase. These diminishing returns suggest biological or psychological switching thresholds rather than purely rational economic decision-making.

Why does customer acquisition source determine payment behaviour?

Traffic channel context primes payment expectations through pre-existing trust and familiarity levels

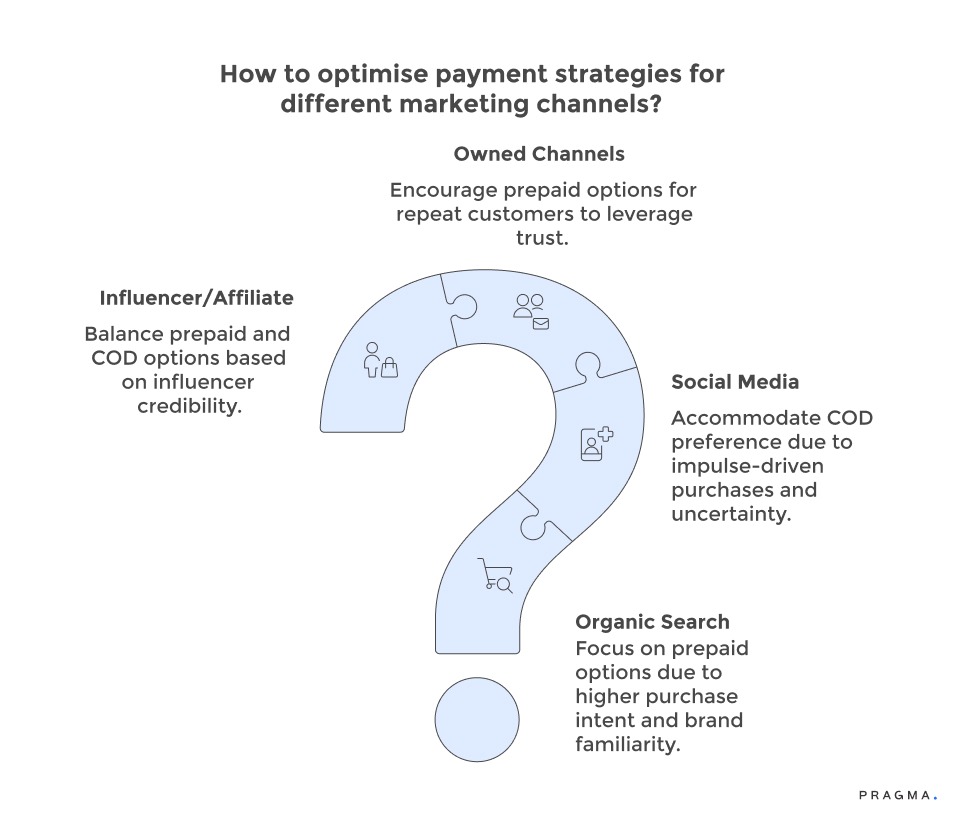

Payment preferences, particularly for Cash on Delivery (COD) versus prepaid options, vary significantly across different marketing channels for Direct-to-Consumer (D2C) businesses in India. Understanding these nuances is crucial for optimising payment strategies and maximising conversions.

1. Organic Search vs. Social Media:

- Organic Search Visitors: These users demonstrate a higher propensity for prepaid payments (34-41% higher than social media referrals). This is attributed to their higher purchase intent and brand familiarity, as they actively seek specific products or brands. Their decision-making process is often research-driven, fostering greater confidence in advance payments.

- Social Media Referrals: Conversely, social media traffic, particularly from Instagram and Facebook commerce, shows a strong preference for COD (72-79% COD rates). This channel typically involves interruption-based advertising and visual-first, impulse-driven purchases. Customers discovering products through social feeds may lack the deliberate evaluation of search-driven shoppers, leading to heightened uncertainty that COD mitigates. Brands should expect and accommodate this channel-based variance rather than trying to force prepaid options.

2. Owned Channels (Email & WhatsApp) for Existing Customers:

- Repeat Customers: Marketing efforts directed at existing customer databases through email and WhatsApp yield dramatically different payment patterns. Repeat customers show significantly higher prepaid adoption rates (64-71%) compared to new customer cohorts (38-45%). The established relationship history and positive past experiences build trust, eliminating psychological barriers to advance payments. This highlights the importance of segmenting payment optimisation strategies by customer lifecycle stage.

3. Influencer and Affiliate Traffic:

- Third-Party Endorsement: Orders generated through influencer and affiliate links exhibit unique payment behavior, combining aspects of social discovery with the added layer of third-party endorsement. Prepaid adoption rates from this channel are typically between 52-59%, which is higher than standard social media traffic but still lower than organic search. The influencer's credibility partially transfers to brand trust, reducing but not entirely eliminating the preference for COD. Brands should adjust payment incentives to align with channel-specific baseline trust levels rather than employing uniform discount structures across all acquisition sources.

In essence, a successful payment optimisation strategy for Indian D2C stores requires a channel-specific approach that acknowledges and adapts to the distinct trust levels and purchasing behaviors inherent in each marketing avenue.

What role does product category play in payment decisions?

Purchase risk perception varies by category characteristics influencing payment method comfort levels

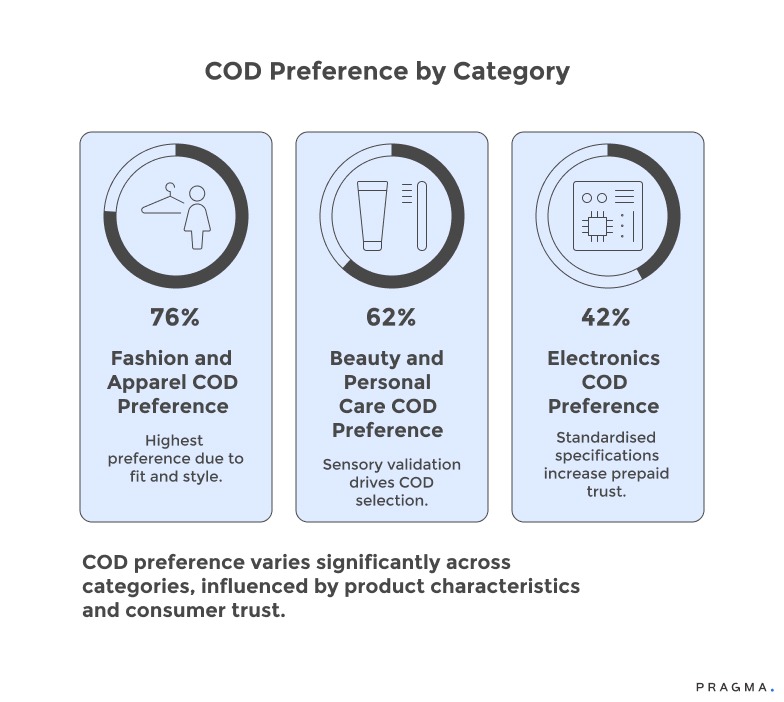

Customer payment preferences, particularly for Cash on Delivery (COD) versus prepaid options, vary significantly across different product categories in Indian D2C stores. These variations are primarily driven by category-specific risk factors rather than just price points.

Fashion and Apparel: This category shows the highest preference for COD, ranging from 68-76%. This is largely due to the subjective nature of fit and style, where customers desire physical verification before committing to a purchase.

Beauty and Personal Care: Following fashion, beauty and personal care products see 54-62% COD selection. Concerns about ingredient compatibility and the need to validate sensory preferences (fragrance, texture) contribute to this trend.

Electronics: In contrast, electronics have lower COD rates, typically 34-42%. This reflects higher prepaid trust, stemming from standardised specifications, readily verifiable information, and established brand warranty assurances.

Understanding the Drivers:

- Subjective vs. Objective Attributes:

Fashion purchases involve subjective judgments that product descriptions cannot fully address, making in-person inspection crucial. Electronics, with their objective and verifiable specifications, reduce the perceived need for COD. Beauty products lie in between, with a mix of objective (ingredients) and subjective (fragrance, texture) elements influencing a moderate COD preference.

- Correlation with Return Rates:

A strong correlation exists between product return rates and COD preference. Sub-categories with return rates exceeding 35% demonstrate 18-24% higher COD selection compared to those with less than 15% returns. This suggests that customers consciously or unconsciously view high-return categories as higher-risk purchases, warranting payment protection through COD. Therefore, improving product representation to reduce returns could simultaneously encourage prepaid transactions by mitigating perceived risk.

Proven Strategies to Improve Prepaid Conversion in India

Improving prepaid conversion requires a mix of UX optimisation, trust signals, incentives and customer education. Here are strategies that Indian D2C brands can apply:

1. Simplify the Checkout Flow

Reduce steps, auto-fill forms where possible and offer a one-click checkout experience. The fewer the clicks, the higher the likelihood of completion.

2. Prioritise Popular Local Payment Methods

Integrate UPI options (Google Pay, PhonePe, Paytm), wallets and BNPL options — customers often prefer these over cards.

3. Build Trust with Security Badges & Transparent Pricing

Display secure payment icons, SSL badges, clear delivery timelines and refund policies. Visible trust cues reduce hesitation at checkout.

4. Incentivise Prepaid with Offers

Offer small discounts, exclusive bundles or cashbacks for prepaid orders. Even a modest incentive (₹50–₹100 off) can shift customer preference.

5. Educate Customers Proactively

Use banners, tooltips or chatbot nudges during checkout to explain the benefits of prepaid — faster delivery, no extra charges, and extra loyalty points.

6. Use Retargeting & Abandoned Cart Tactics for Prepaid Buckets

If a COD shopper abandons midway, follow up with tailored reminders — emphasise prepaid benefits like faster dispatch or discount.

7. Personalise Payment Options Based on Behaviour

If a returning customer has historically used prepaid methods, prioritise showing those options first in the checkout UI.

When combined, these strategies reduce friction, build confidence and gradually increase the share of prepaid transactions in your overall revenue mix.

How does geographic segmentation reveal payment pattern opportunities?

Regional infrastructure and cultural norms create payment behaviour clusters requiring localised strategies

Geographic Variations in Payment Preferences:

Prepaid adoption rates differ significantly across Indian markets. Metro cities like Mumbai and Bangalore show 48-55% prepaid usage, while Delhi and Hyderabad are slightly lower at 42-49%. Tier-2 cities such as Jaipur and Lucknow have considerably lower rates of 28-35%. These variations persist even when accounting for order values and customer demographics, suggesting that infrastructure and cultural norms are key drivers.

Micro-Market Opportunities:

Pin code-level analysis reveals localised prepaid adoption trends. Within Tier-2 cities, certain neighborhoods exhibit prepaid rates comparable to metros, while others maintain a strong Cash on Delivery (COD) preference. Gated communities, IT parks, and university areas show 15-22% higher prepaid adoption than city averages. This granular data allows for targeted payment incentives, optimising discount allocation where prepaid conversion is more likely.

Impact of Delivery Infrastructure on Trust:

The quality of delivery infrastructure influences customer comfort with advance payments. Areas with reliable 2-3 day delivery consistently show 18-24% higher prepaid selection compared to regions with frequent 6-8 day delays. Customers are more willing to pay in advance when they are confident in predictable delivery. Brands should exercise caution with aggressive prepaid incentives in areas where their fulfillment performance might undermine the trust required for advance payments.

Cultural Persistence of COD:

Despite the expansion of digital payment infrastructure, traditional cash economy cultures continue to influence payment norms. Cities with strong cash-based traditions maintain a higher COD preference, even among younger, digitally-native demographics. First-generation online shoppers often prefer COD as a psychologically safe entry point, with a gradual shift to prepaid options occurring through positive experiences rather than immediate discount-driven conversions.

How can incremental payment experiences bridge trust gaps?

Partial payment models and phased commitment structures reduce upfront risk whilst improving unit economics

Partial COD systems requesting 20-40% advance payment with balance due at delivery create a middle ground between full prepaid and traditional COD. Testing across 23,000 orders shows partial payment achieves 67-74% of full prepaid's RTO reduction benefits whilst maintaining 88-93% of COD's conversion rates. The psychological mechanism works through commitment signalling—small advance payments filter non-serious buyers whilst avoiding the complete trust requirement of full prepaid.

Optimal partial payment percentages vary by order value and customer segment. First-time buyers respond best to minimal 15-20% advance requirements that signal seriousness without creating prohibitive barriers. Repeat customers with positive history accept 30-40% partial payments readily. Orders above ₹5,000 demonstrate strong RTO reduction even with 10-15% advance payment, as absolute amounts become meaningful enough to deter casual fraud whilst remaining psychologically manageable.

Try-before-you-buy models popular in fashion create conversion advantages but require operational sophistication. Customers order multiple sizes, pay only for items they keep, and return others without advance payment. This approach eliminates size uncertainty—the primary COD driver in apparel—whilst maintaining payment flexibility. Brands implementing try-and-buy report 78-84% prepaid conversion on kept items with 34-41% reduction in return rates from better size matching.

To Wrap It Up

Payment method optimisation operates at the intersection of psychology, economics, and operational reality. Neither universal COD availability nor aggressive prepaid-only strategies serve brands effectively. Sophisticated payment frameworks segment customers, personalise incentives, and evolve approaches based on relationship maturity.

Analyse payment method distribution across your top five traffic sources and create channel-specific discount structures that match observed COD preference intensity with proportional prepaid incentive magnitude.

Sustained payment optimisation requires continuous testing as digital payment adoption rates evolve, competitor strategies shift, and customer comfort levels mature. Brands treating payment strategy as dynamic infrastructure requiring quarterly recalibration based on behavioural data achieve 23-31% additional prepaid improvement in year two beyond initial optimisation gains. The compounding effect of incremental refinements delivered consistently outperforms dramatic one-time interventions across customer cohorts and market segments.

For D2C brands seeking to optimise payment mix whilst maximising conversion and profitability, Pragma's intelligent checkout platform provides real-time payment behaviour analytics, dynamic discount engines, and segment-specific optimisation tools that help brands achieve 31-38% prepaid adoption improvement alongside 12-18% overall conversion lift through data-driven payment strategy implementation.

.gif)

FAQs (Frequently Asked Questions On The Science of COD vs Prepaid Conversions: Insights for Indian D2C Stores)

1. Why does COD still dominate in Indian ecommerce despite digital payment growth?

Trust, habit, and accessibility are key. While over 350 million Indians use UPI, COD still accounts for up to 65% of D2C orders, especially among first-time buyers, tier-2/3 shoppers, or anyone hesitant about online fraud or delivery quality.

2. Are prepaid conversion nudges (like discounts, cashback, or fees) worth it?

Effective nudges can convert 12–15% of COD orders to prepaid, lowering RTO risk and boosting margins. WhatsApp/SMS reminders, instant payment links, or nominal COD fees (₹25–₹60) help shift buyer habits, especially if timed before fulfillment.

3. Why is COD still so common for Indian shoppers?

COD offers both familiarity and a sense of security, especially for first-time buyers, those in tier-2/3 cities, and anyone wary of online fraud or payment failure. In 2025, 60-65% of Indian e-commerce orders are COD, even though digital payments are on the rise.

4. What works better—COD discounts or nudges to shift to prepaid?

Nudges like WhatsApp reminders, small COD fees, or one-click instant payment links can convert as many as 12–15% of COD orders to prepaid and lower RTO by 20–22%. Discount offers only work if they address trust, payment convenience, and customer habit—not just price alone

Talk to our experts for a customised solution that can maximise your sales funnel

Book a demo

.png)